Chips, Broader Market Up Early on Peace Talk Hopes

Published as of: July 20, 2026, 9:14 a.m. ET

Listen to this update

Listen here or subscribe to the Schwab Market Update in your favorite podcast app.

| The markets | Last price | Change | % change |

|---|---|---|---|

| S&P 500® Index | 7,457.69 | -76.08 | -1.01% |

| Dow Jones Industrial Average® | 52,146.42 | -406.55 | -0.77% |

| Nasdaq Composite® | 25,520.24 | -361.70 | -1.40% |

| 10-year Treasury yield | 4.56% | +0.02 | -- |

| U.S. Dollar Index | 100.87 | +0.11 | +0.11% |

| Cboe Volatility Index® | 18.09 | -0.67 | -3.57% |

| WTI Crude Oil | $82.56 | +$0.07 | +0.08% |

| Bitcoin | $64,750 | +$480 | +0.76% |

(Monday market open) Crude oil wobbled and major indexes climbed to start the week after Iran said it might be willing to pursue diplomacy, The Wall Street Journal reported. Early gains after a weekend of Middle East escalation included chip stocks approaching a host of earnings that could help set direction for the struggling sector.

"Technically, we're oversold in the Nasdaq-100® and the PHLX Semiconductor Index (SOX), so it wouldn’t surprise me to see some mean reversion at some point this week, especially if Alphabet announces strong, or increased, CapEx guidance," said Nathan Peterson, director of derivatives research and strategy at the Schwab Center for Financial Research (SCFR), writing in Schwab's Weekly Trader's Outlook.

Wall Street cratered Friday and sector action was dismal, with only energy up as oil price fears gripped the market and fighting escalated with nine straight days of U.S. strikes. Major indexes fell across the board last week, though Treasury yields eased slightly. The Federal Reserve enters its quiet period ahead of next week's meeting. As of early today, chances of a rate pause are 88%, according to the CME FedWatch Tool. "We expect the Fed to remain on hold for the next handful of meetings," said Collin Martin, head of fixed income research and strategy at SCFR.

To get the Schwab Market Update in your inbox every morning, subscribe on Schwab.com.

Three things to watch

- South Korea's volatility reverberates in U.S. chip sector: South Korea's major index has become "effectively a barometer for the AI trade," said Michelle Gibley, director of international equity research and strategy at SCFR. She cited issues including the position that memory chips have as a bottleneck in the AI supply chain, explosive growth in profits, the large market cap of companies domiciled there, and growth of leveraged single stock ETFs. South Korea tried to reduce the influence of leveraged ETFs, halting new listings last week to cool what Bloomberg called a "trading frenzy." South Korea's rate hike last week also hurt stocks there and weakness traveled across the Pacific, reinforcing how global developments can play out here. Stocks in South Korea slumped again to start the week as Samsung reportedly cut jobs, CNBC reported. Another weight on chips and tech in general is muscle memory. Market participants have frequently punished hyperscalers at earnings time for swollen spending forecasts and taking on new debt, also contributing to recent frayed nerves on Wall Street. Alphabet (GOOGL) and Intel are the next guideposts later this week after investors punished ASML (ASML) and Taiwan Semiconductor Manufacturing (TSM) last week despite strong results and guidance.

- Key chip firms don't factor into S&P 500 earnings growth: Second quarter S&P 500 earnings per share for the approximately 10% of S&P 500 firms that had reported through Friday grew an eye-popping 52%, and that figure didn't even include TSM or ASML. Neither is a member of the S&P 500, which might surprise those reading regularly about these two chip industry giants and their heavy influence on U.S. markets. Both companies are American Depositary Receipt (ADR) firms, which offer U.S. investors a chance to include international stocks in their portfolios. They are negotiable securities but don't represent direct ownership in a company. Instead, they're certificates issued by a U.S. bank corresponding to shares of a non-U.S. company. ADRs of TSM trade on the New York Stock Exchange. ASML's ADR trades on the Nasdaq. "These stocks are not impacting your SPY or S&P 500 fund, but obviously, if ASML or TSM are moving big one way or the other, that's going to affect the chip companies in the S&P 500 since they typically trade as a cohort," Peterson said.

- Leading indicators, TIPS auction ahead: Treasury note yields eased last week but remain elevated. June leading indicators today and S&P Global manufacturing updates later this week are among coming reports that could move the bond market. The leading indicators index "hasn't done a very good job giving a heads-up as to the direction for the economy," said Liz Ann Sonders, chief investment strategist at SCFR, in Friday's OnInvesting podcast. "It's kind of flashed recession for a few years now, but interestingly it just started to tick a little bit higher. So I'll be looking to see whether that improving trend has legs." Another element this week is a 10-year Treasury Inflation Protected Securities (TIPS) auction, which could hint at how much demand there is for inflation protection.

On the move

- Domino's Pizza (DPZ) heated up nearly 8% even though earnings per share missed analysts' estimates. Revenue topped expectations, however, and order count rose, which the company said is the most important driver of long-term success.

- Chinese stocks rose overnight on continued support from Friday's release of an AI model from Moonshot AI, which contributed to last Friday's global AI market pressure. China's Kimi K3 large language model could outperform cutting-edge U.S. systems, The Wall Street Journal reported.

- Alibaba (BABA) climbed 3.4% in early trading. The Chinese firm unveiled a preview version of its flagship large language model (LLM), Qwen3.8 Max. Separately, the Trump administration is considering banning Chinese AI models, Axios reported today.

- The SOX climbed 2% this morning. It lost 1.63% Friday and entered bear territory, defined as a drop of 20% or more from the last market peak. SOX fell around 10% last week alone. Early chip and AI leaders Monday included SK Hynix (SKHY), Micron (MU), and Western Digital (WDC), all up 4% or more.

- Paramount Skydance (PSKY) dropped 4% this morning. Investors await a judge's ruling expected by Wednesday on 12 state lawsuits against its merger with Warner Bros Discovery (WBD). The states say the merger could hurt competition.

- AMC Entertainment (AMC) soared 16% this morning after a blockbuster opening weekend for "The Odyssey" and quarterly earnings that beat estimates.

- Urban Outfitters (URBN) climbed nearly 5% on an upgrade to buy from neutral at Goldman Sachs, saying Anthropologie brand execution risk is now embedded in expectations.

- Travelers Companies (TRV) climbed more than 9% Friday after earnings and revenue topped estimates. The company cited strong underwriting results.

- Rotation earlier last week that saw Magnificent Seven and cyclical names gain ground versus chips flagged Friday. Small caps fell along with their mega-cap brethren. The S&P 500 Equal Weight Index (SPXEW), which easily outpaced the S&P 500 Index Thursday, struggled Friday.

- SpaceX (SPCX) retreated 5.4% Friday and stayed below its $135 initial public offering (IPO) price. The latest drop came after the company aborted the launch of a Starship rocket. Shares rose 1% this morning as the company announced it would try to relaunch as early as Thursday.

- The global crude benchmark price climbed 4% Friday and 14% last week but remains below spring highs, hinting investors expect a return to relative calm. An extended conflict might put supplies in worse shape than earlier in the war, as stockpiles are thinner globally. After falling early today on hopes for peace talks, oil rebounded on media reports that Yemen's Houthi rebels declared a maritime embargo of Saudi Arabia that could affect Red Sea oil shipments.

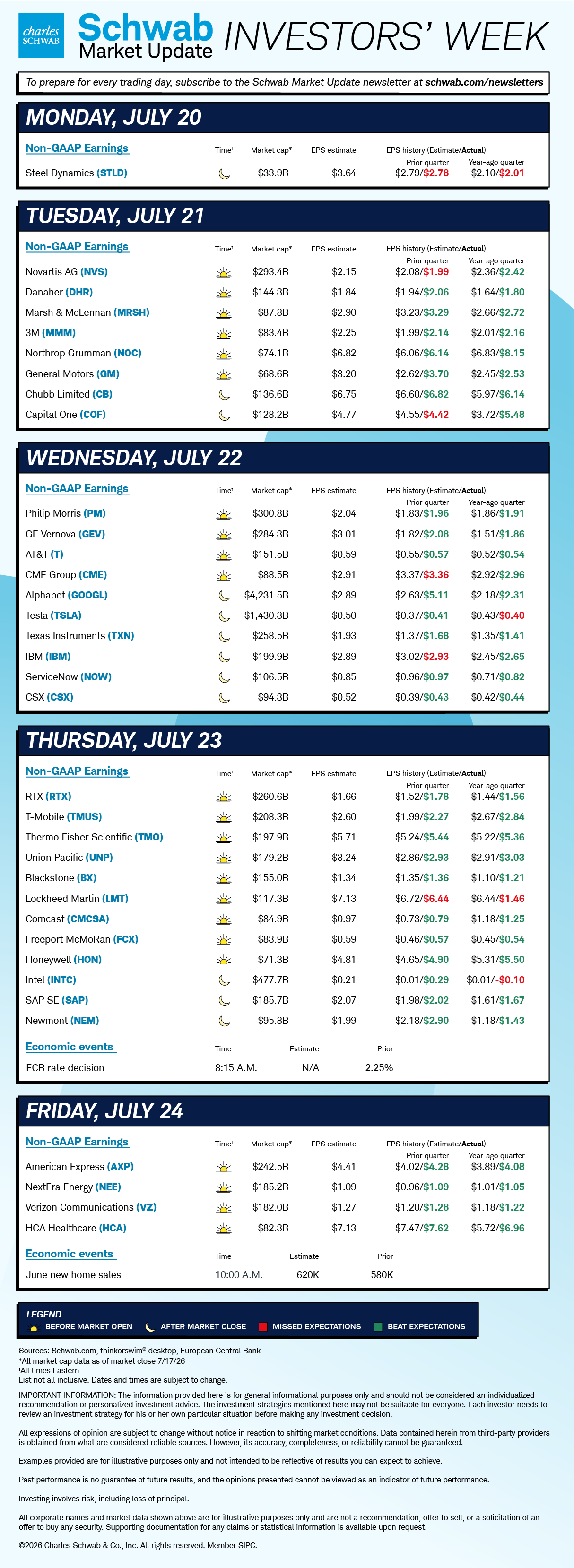

- FactSet raised its earnings growth estimate to 24.7% for S&P 500 companies. "Second quarter results have been tracking exceptionally well, although it's early," my colleague Peterson said. About 15% of S&P 500 firms report this week including General Motors (GM), IBM (IBM), and Tesla (TSLA).

More insights from Schwab

Schwab's latest big picture view: According to the new Schwab Market Perspective, strong corporate earnings may continue to support global stocks, but concentration risks remain. What's unusual about the recent earnings strength is that it is occurring outside a typical early-cycle recovery period. The report focuses on what appears to be a new era characterized by more volatility.

The decision making behind investing: There's more to it than just choosing what investments go in a portfolio. Making smart decisions has to do with managing behavior, which SCFR's Mark Riepe discussed with Kasy McCurdy, chief portfolio strategist at SCFR, in the latest episode of Financial Decoder.

Chart of the day

Data source: Nasdaq. Chart source: thinkorswim® platform.

Past performance is no guarantee of future results.

For illustrative purposes only.

The tech-heavy Nasdaq-100 index (NDX—candlesticks) fell below its 50-day moving average (blue line) last week and is now trading at its lowest level below that line since early April. The intraday low for the NDX back on June 9 was roughly 28,200, and this is the same level where buyers stepped in Friday, so that could be considered near-term support. However, the index lost support at its 50-day simple moving average last week which is bearish technically.

The week ahead