Tech Malaise Persists Amid AI Cost, Spending Fears

Published as of: June 26, 2026, 9:15 a.m. ET

Listen to this update

Listen here or subscribe to the Schwab Market Update in your favorite podcast app.

| The markets | Last price | Change | % change |

|---|---|---|---|

| S&P 500® Index | 7,357.49 | -0.73 | -0.01% |

| Dow Jones Industrial Average® | 51,920.62 | +71.72 | +0.14% |

| Nasdaq Composite® | 25,358.60 | -118.03 | -0.46% |

| 10-year Treasury yield | 4.39% | +0.02 | -- |

| U.S. Dollar Index | 101.20 | -0.22 | -0.23% |

| Cboe Volatility Index® | 20.12 | +1.23 | +6.56% |

| WTI Crude Oil | $69.55 | -$2.37 | -3.30% |

| Bitcoin | $59,470 | +$35 | +0.06% |

(Friday market open) Technology stocks can't catch a break this week despite robust earnings from chip giant Micron (MU). Though major indexes retreated early today as tech sagged again—and are on pace for weekly losses—advancing shares keep outnumbering declining ones. This suggests investors are rotating their money into sectors beyond tech, a potentially healthy development even as mega caps lose ground on worries about spiraling AI costs and a possible delay in OpenAI's initial public offering.

Today's calendar is relatively light, but investors may want to track final University of Michigan Consumer Sentiment due soon after the open. Consensus is for a headline figure of 48.9%, unchanged from the initial estimate and near historic lows, according to Briefing.com. Inflation expectations are also worth tracking. July starts with a bang next week thanks to jobs data, including next Thursday's nonfarm payrolls report. Early forecasts suggest June jobs growth eased significantly from May's surprisingly robust 172,000.

Major indexes again went separate ways Thursday. The Nasdaq Composite dropped, the S&P 500 Index ended flat, and the Dow Jones Industrial Average and the Russell 2000® Index (RUT) gained. Six of 11 S&P 500 sectors rose, mirroring Wednesday's results with sectors like industrials and energy in the green. Health care has rallied amid some rotation into weaker areas. Some of Wall Street's softness could reflect consolidation after the spring rally. Funds may be trimming exposure to equities in a quarter-end rebalancing move.

To get the Schwab Market Update in your inbox every morning, subscribe on Schwab.com.

Three things to watch

- Wedge seen in tech sector: Good news for Micron isn't necessarily great for tech in general. Micron and its competitors keep improving their results thanks to the rising cost of the memory chips used in products from phones to laptops to automobiles. As Briefing.com noted Thursday, this could potentially reinforce a growing wedge in the tech sector so far this year, with memory chip names like Micron far surpassing gains of "hyperscaler" stocks like Microsoft (MSFT), Amazon (AMZN), and Alphabet (GOOGL). The latter three spend heavily on chips and face rising costs as they try to grow their AI data centers. Shares of Apple (AAPL) dove Thursday on margin concerns after it announced price increases for several iPad and Mac models, citing higher costs from memory chip shortages. Those high costs are seen persisting throughout 2027 and perhaps into 2028, analysts say, driven by increasing data center demand and by Nvidia's (NVDA) rapid introduction of updated AI chips, with each new cycle requiring more memory. As Micron and its cohorts scramble to meet the needs of Nvidia, hyperscalers find the competition for chips intensifying.

- Breadth improves as yields fall: One slightly encouraging feature this week is that advancing shares outnumbered decliners in the S&P 500 Index even on Tuesday and Wednesday when the overall index fell. This has driven improved breadth as investors gravitate out of tech and into other sectors. Normally, that's a healthy development because it suggests the market might not depend so much on a narrow sliver of stocks to propel things higher. If Treasury yields keep declining, it could potentially reinforce this trend by lowering borrowing costs, helping consumer spending. Though the recent yield drop won't necessarily last and may depend partly on volatile oil prices, it presents some hope for sectors like industrials and discretionary. By late Thursday, 63% of S&P 500 stocks traded above their 50-day moving average, up from 50% at the start of June. The rolling 52-week correlation between the cap-weighted and equal-weighted S&P 500 indexes is plunging and at its lowest since 2003, noted Kevin Gordon, head of macro research and strategy at the Schwab Center for Financial Research (SCFR).

- Credit check: Behind the scenes, credit markets continue to perform well, with spreads low across the board thanks to a resilient economy and strong earnings. "Supply and demand could pose a risk as investment grade corporate bond issuance is expected to set a monthly record this month," said Collin Martin, head of fixed income research and strategy at SCFR. "Unless demand keeps up with supply, spreads may need to move a bit higher to attract new investors. We view that as a short-term technical risk rather than a risk of a sustained move higher in credit spreads." Credit spreads sometimes rise before the stock market begins to show signs of cracking, so they can be an important indicator for stock investors to watch. If things are good for the economy, investors generally don't demand much spread. If the outlook changes, investors could get nervous and demand additional yield.

On the move

- Memory chip stocks including Micron (MU) retreated early today after blockbuster gains for SanDisk (SNDK) and Micron Thursday. Micron was down 4.7% ahead of the open and SanDisk lost nearly 5%. This followed overnight weakness in South Korea's semiconductor-dominated stock market.

- Other tech stocks including Oracle (ORCL) and CoreWeave (CRWV) fellahead of the open after The New York Times reported that OpenAI might be poised to wait until next year to present its initial public offering (IPO). Executives at OpenAI may shift from an earlier IPO due to choppy global markets and struggles for SpaceX (SPCX) shares after its IPO earlier this month, the newspaper reported.

- Chip infrastructure firms like Lumentum (LITE), Marvell Technology (MRVL), and Corning (GLW) were also down moderately early today.

- ON Semiconductor (ON) plunged 14% early today after agreeing to buy Synaptics (SYNA), a company that specializes in custom-designed human interface. Shares of Synaptics rose 3.7%. ON makes chips for automotive and industrial markets. It's an all-stock deal worth $7 billion.

- Nvidia (NVDA) slipped another 1% early today and is on pace for an 8% decline this week, its worst week in more than a year. This reflects competition from memory stocks for investor money and worries about the pace of AI spending, Barron's reported.

- Apple (AAPL) fell 6% Thursday to post its worst day in more than a year after announcing price increases. Shares edged up today. Microsoft (MSFT) sagged 3% Thursday after it raised Xbox prices. Both might be struggling with their margins as the cost of memory chips continues rising. Early today, CNBC reported that Apple could turn to Chinese memory makers amid AI-driven supply shortages.

- With mega caps under pressure, investors appeared to steer toward old-fashioned U.S. industrials like Caterpillar (CAT) and Deere (DE) on Thursday. They rose 6.3% and 5%, respectively. Transport names including railroads and airlines also provided some muscle.

- The Russell 2000 led all major indexes yesterday with moderate gains, but things could get choppy later today both for small- and large-caps as FTSE Russell performs its semi-annual rebalancing after the close. This could have dramatic effects in terms of asset weighting as companies are added and subtracted from FTSE Russell's indexes and new weights are assigned.

- Crude oil (/CL) declined 2.7% ahead of the open despite yesterday's Iranian attack on a ship traversing the Strait of Hormuz. That sent oil higher Thursday afternoon and reinforced how tentative the 60-day ceasefire might be.

- Technically, the S&P 500 managed to claw back in the final minutes Thursday to finish just a hair above its 50-day moving average of 7,356. It hasn't closed below that line since early April but has threatened to for three straight sessions. Several successive settlements below it would likely be needed to confirm a bearish turn.

- The S&P 500 Equal Weight Index (SPXEW) easily outpaced the S&P 500 Index yesterday and is up over the last week. It weighs all components equally rather than by market capitalization, making it less exposed to mega-cap declines.

- With three trading days left, the S&P 500 Index is down 3% in June after surging in April and May. The Nasdaq is down four straight days.

More insights from Schwab

The dollar, the Fed, chips, and more: In their latest On Investing podcast, Schwab experts discussed recent dollar strength, the direction of long-term Treasury yields, and the "chip dip" that has the PHLX Semiconductor Index (SOX) verging on correction territory down almost 10%. They also assess the quick sector rotation shifts characterizing recent market action.

" id="body_disclosure--media_disclosure--174046" >The dollar, the Fed, chips, and more: In their latest On Investing podcast, Schwab experts discussed recent dollar strength, the direction of long-term Treasury yields, and the "chip dip" that has the PHLX Semiconductor Index (SOX) verging on correction territory down almost 10%. They also assess the quick sector rotation shifts characterizing recent market action.

How to properly close out a multi-leg option: Traders who follow the step-by-step process outlined in Schwab's new options video might be able to avoid leaving themselves in an unintended position with unintended risk.

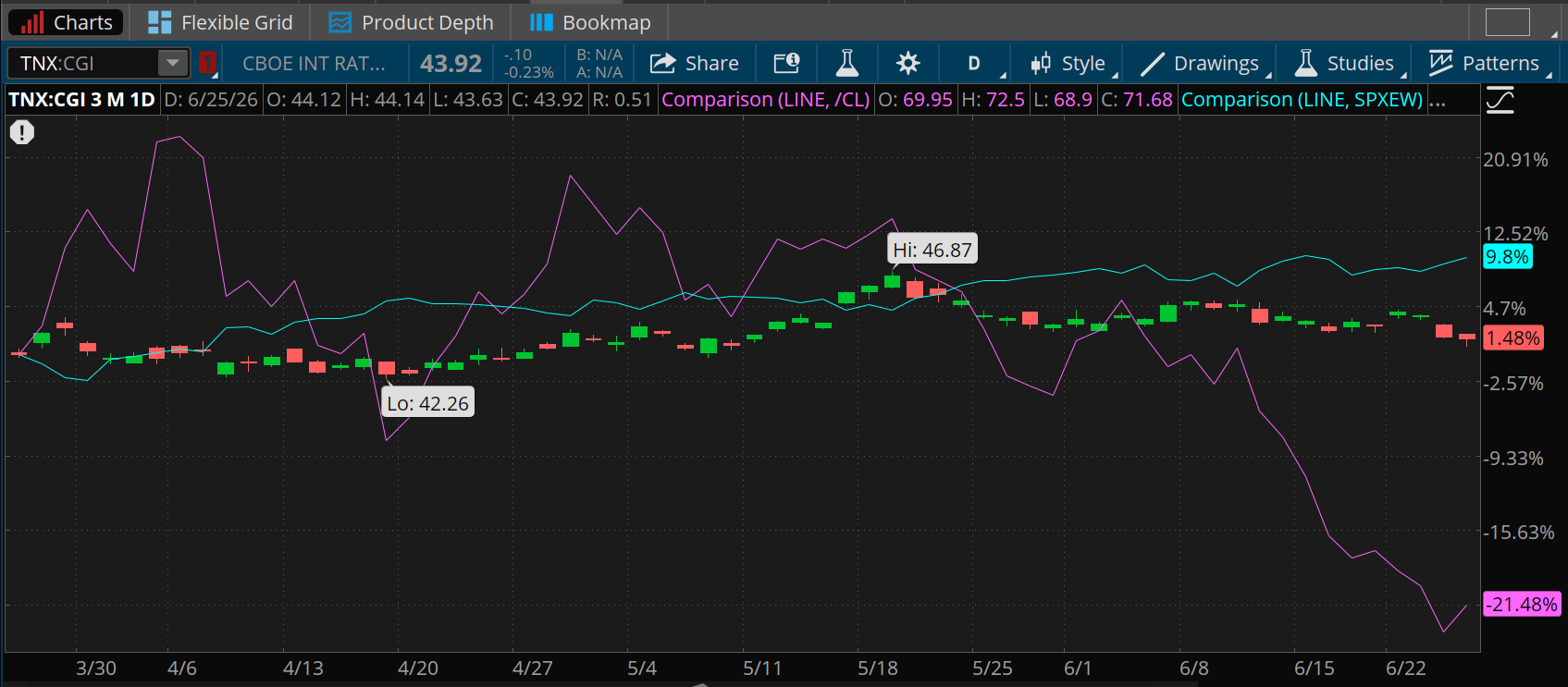

Chart of the day

Data source: Cboe, S&P Dow Jones Indices, CME Group. Chart source: thinkorswim® platform.

Past performance is no guarantee of future results.

For illustrative purposes only.

Though the Nasdaq and S&P 500 Index have struggled recently, falling prices of crude oil (/CL—purple line) and a slight dip in the 10-year note yield (TNX:CGI—candlesticks) gave the S&P 500 Equal Weight Index (blue line) a recent boost. Though it's still behind the better-known S&P 500 Index (SPX) over this stretch, the SPXEW showed new strength this week, rising 0.7% Thursday even as the SPX finished slightly lower. This shows up in better market breadth.

The week ahead

June 29: No major earnings or data expected.

June 30: June consumer confidence, May job openings and labor turnover survey (JOLTS), and expected earnings from Nike (NKE) and Constellation Brands (STZ).

July 1: ADP June employment change, June construction spending, June ISM Manufacturing PMI®, and expected earnings from General Mills (GIS).

July 2: June nonfarm payrolls, June unemployment, June hourly earnings, and June factory orders.

July 3: U.S. markets closed for Independence Day.