Emerging Markets: AI Opportunity and AI Risk

Key takeaways:

- Emerging-market (EM) stock prospects could be supported by an acceleration in global gross domestic product (GDP) growth and a weak dollar, but EM stocks also have the opportunities and risks associated with the growth in artificial intelligence (AI).

- EM stocks now have a technology and AI focus due to the optimism toward Chinese AI enablers and adopters as well as the global buildout of AI.

- Estimates of future earnings for the MSCI Emerging Market (EM) Index have jumped in conjunction with AI-driven optimism, keeping equity valuations attractive. The risks of AI have also grown, which may prove to be a headwind toward achieving those higher earnings targets.

We reiterate the view in our 2026 outlook that both developed and emerging-market international stocks could see another year of strong returns. Earnings and economic growth are expected to accelerate, stocks are attractively valued relative to the S&P 500 index and a weak U.S. dollar could support higher returns. Given the impact AI initiatives are having on emerging markets, it's worth a deeper dive into both the opportunities and risks.

EM companies are increasingly AI companies

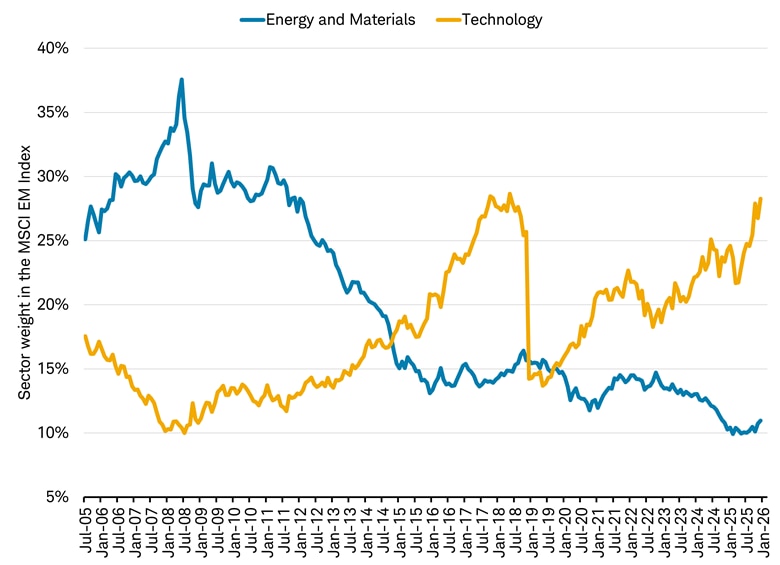

Twenty years ago, the MSCI EM Index had a bias toward commodities sectors such as Energy and Materials. Over the past 20 years, it transitioned toward a technology focus, as seen in the chart below. The weight of the Information Technology sector dropped with the reclassification of internet-related companies into Communication Services and Consumer Discretionary sectors in late 2018, but regained lost ground over recent years.

The EM stock index has become tech-focused

Source: Charles Schwab, MSCI, as of 1/6/2026.

Sectors are based on the Global Industry Classification Standard (GICS®), an industry analysis framework developed by MSCI and S&P Dow Jones Indices to provide investors with consistent industry definitions. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

The Technology sector is a major factor in the market performance for three of the top four largest country weights in the MSCI Emerging Market (EM) Index. These countries and their weights as of December 31, 2025, are China (27.6%), Taiwan (20.6%), and South Korea (13.3%). India is not driven by the technology sector but is the third-largest weight at 15.3% weight. Companies in these four countries make up over three-quarters of the index and drive its overall performance.

As the largest country weight, let's look at Chinese stocks. The MSCI China Index has a roughly 50% weight in technology and internet-related companies across the Communication Services, Consumer Discretionary, and Information Technology sectors. Most primarily sell to the domestic Chinese market. Although internet-related companies within the Consumer Discretionary sector of the MSCI China Index have struggled in recent years with depressed consumer confidence and low profit margins due to excessive competition (called "involution" in China ), there are hopes the crackdown on disorderly price competition via the anti-involution campaign of China's government could help to increase profits. Additionally, internet companies in China are quickly becoming AI adopters, incorporating AI models and software technologies in their operations and/or generating revenue from AI models, which has the potential for increased sales growth and higher profit margins via increased efficiency.

The release of the AI model DeepSeek R1 in January 2025 brought attention to the innovation that has been happening within Chinese companies over many years. DeepSeek was able to make similar technological progress to AI-related companies located in the U.S., with reportedly much lower capital requirements. This optimism around AI has resulted in a number of Chinese companies recently going public, often resulting in eye-popping one-day stock returns per Bloomberg. There may be hope that with more capital, Chinese AI companies could make further advances in the field. However, any enthusiasm for AI initial public offerings (IPOs) in China may be overdone if profits don't follow. It's likely too early to know if excess capacity and involution will become a problem for Chinese AI companies, similar to other industries that in the past have experienced a rush of investment which resulted in downward pressure on profit margins.

In Taiwan and South Korea, several large market capitalization semiconductor companies in the supply chain for the global rollout of AI infrastructure and data centers (AI enablers, or firms providing the infrastructure needed to train and generate revenue from AI models) drove gains in earnings growth and market performance in 2025. South Korea also has an improving corporate governance story, similar to recent reforms in Japan. The Korean government's "Corporate Value-Up" reforms have the potential to make Korean businesses more friendly to outside shareholders and reduce the valuation discount these primarily family-owned conglomerates typically receive relative to global peers.

India has less exposure to the AI buildout theme. With financials and consumer discretionary the top sectors in the MSCI India Index, it is primarily a domestic economic growth story, and its technology services industry could be hurt by AI if labor is replaced by increased AI adoption. India's economy has been weighed down by high inflation, but it has likely peaked for this cycle. In 2025, interest rates started to be cut by the country's central bank, the Reserve Bank of India, which may help stabilize economic growth and earnings going forward, but for now, earnings estimates have continued to be revised lower.

AI brings risks for EM companies

The global enthusiasm for AI growth comes with opportunities in emerging markets, but also plenty of risks. Specifically, the Chinese government has made AI leadership a priority and can invest directly into companies, build electricity infrastructure, subsidize energy costs, and move fast on AI regulations. However, China's restrictions on sensitive political issues may limit AI model inputs and result in answers that are incomplete or biased. Loose enforcement of copyright laws in China may subject content creators to infringement of their intellectual property, reducing their potential profits and result in less original content. Export controls placed by the U.S. and others on cutting-edge technology could hinder China's ability to keep pace with the rest of the world without further advancement of its domestic chip and semiconductor capital equipment companies.

Emerging-market AI companies with global end markets have similar risks to U.S. and other developed-market AI companies. These include concerns around circular financing, an increased use of debt to fund capital expenditures (capex), questions about the return on investment (ROI), availability of electricity and a mismatch of depreciation costs over a longer period than the useful life of equipment. Advances in technology may solve some of the cost, ROI and need-for-electricity concerns, but could also reduce the potential available market size for some of the companies. Additionally, while difficult to forecast, we believe that Taiwanese companies could be at a low—but non-zero—risk of potential Chinese military aggression.

Earnings have been growing, helping to keep valuations attractive

Optimism about the prospects of AI enablers and AI adopters has likely increased the consensus forecast for the next-12-month forward earnings within the MSCI EM Index, which hit a 10-year high recently, as you can see in the chart below.

EM estimated earnings have jumped over the past year

Source: Charles Schwab, MSCI, FactSet, as of 1/6/2026.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. Past performance is no guarantee of future results.

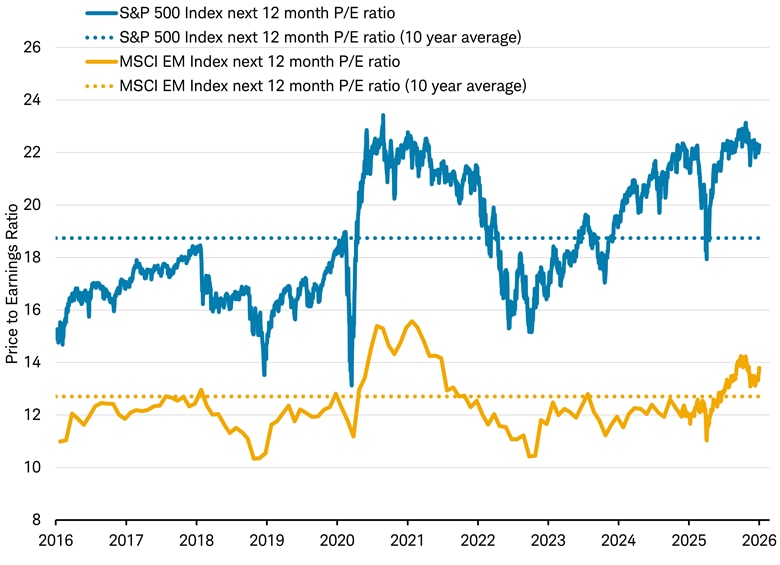

Emerging-market stocks outperformed in 2025, with the MSCI EM Index posting a 34.3% return versus 17.9% for the S&P 500 index per Bloomberg. Despite this, as seen in the chart below, the MSCI EM Index is currently trading at a 13.7x price-to-earnings ratio (P/E), meaning investors are paying $13.70 for every $1 of earnings, only slightly above its longer-term average. Meanwhile, the S&P 500 is trading at a P/E ratio of 22.1x, much higher than its longer-term average. While emerging-market stock valuations as a whole are trading at a discount to the S&P 500, as seen in the chart below, there is the risk that earnings estimates have become too optimistic. If expected earnings are reduced, the P/E could suddenly become much larger, blunting investor appetite for companies with higher valuations and lower earnings prospects.

Emerging markets offer global AI exposure at a lower valuation

Source: Charles Schwab, MSCI, FactSet, as of 1/6/2026.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. Past performance is no guarantee of future results.

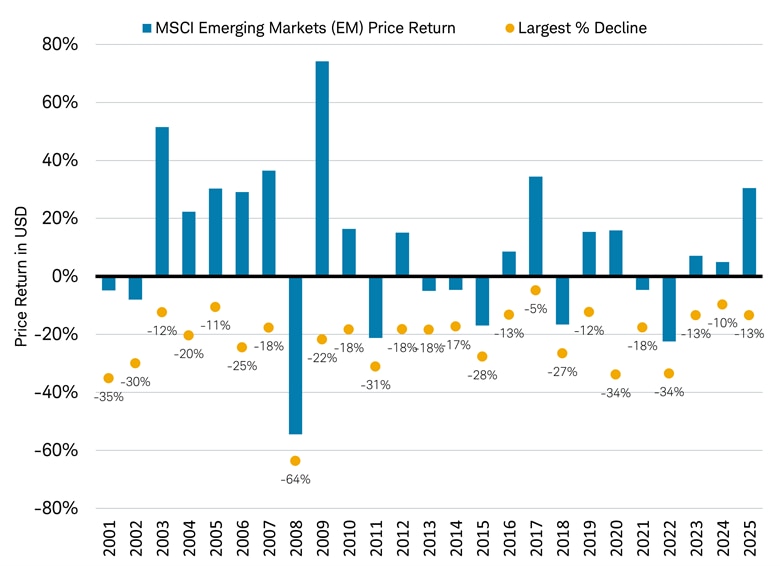

Emerging-market stocks have had a historical tendency to be volatile. Over the past 25 years, the MSCI EM Index has had a 10%-20% decline (considered correction territory) 13 times and a drop of greater than 20% (considered a bear market) 11 times, leaving just one year with a decrease of less than 10%. The potential for greater volatility is one reason investors should consider keeping EM allocations small.

Declines of 10% are not uncommon for the MSCI EM Index

Source: Charles Schwab, Bloomberg data retrieved 1/6/2026.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

In sum

EM stocks have increasingly become tied to the fortunes and risks of the growth in AI. Should the AI capex race continue, and earnings estimates are realized, EM stocks have the potential to continue to rise, because valuations are not yet extended. However, the AI investment theme comes with risks to earnings prospects in emerging markets and globally. We believe EM deserves a small allocation in investor portfolios, but caution that the more EM acts like a tech stock, the less diversification benefit it may provide relative to U.S. stocks.

Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.