Will the United States Dollar Be Dethroned?

Over the years, there have been predictions that the United States dollar is on the verge of a major decline and might even lose its status as the world's major reserve currency. Recent trade conflicts have reignited this speculation. Countries facing economic pressure from tariffs, or the threat of tariffs, are discussing moving away from the dollar as the primary currency for trade. "De-dollarization," or the shift away from using the U.S. dollar as the primary currency of exchange in global trade and investment, has once again become a hot topic in financial markets.

Our view is that while a long-term trend toward greater currency diversification in global financial transactions may continue, it's a big leap from dollar dominance to the loss of reserve currency status.

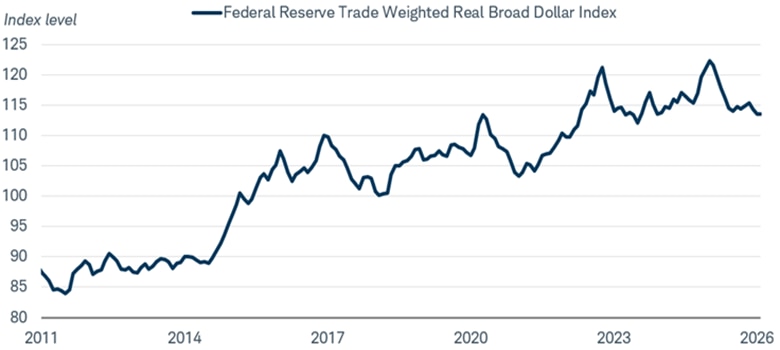

As shown in the chart below, the trade weighted dollar remains near the high end of its 15-year range, despite its decline from the early 2025 peak versus currencies of countries with which the U.S. trades. It also remains the primary currency used for trade and financial transactions in the global economy. The size of the recent non-dollar transactions that have raised concerns are very small. Trade in the Chinese yuan accounted for less than 4% of global trade as of November 2025.1

There are few signs that major foreign holders are poised to suddenly shift away from U.S. dollars and there are few other currencies that could take its place as a reserve currency. In our view, a gradual move to a global economy with a less-dominant dollar is possible over time, but we don't see the dollar losing its reserve currency status.

The U.S. dollar boasts a decade-long bull market

There are several ways to measure changes in the level of the dollar. We generally look at indices that compare the dollar's value to the values of a broad range of currencies, weighted according to the value of their trade with the U.S.

As you can see in the chart below, during the past decade, the dollar has been propelled higher by relatively high U.S. interest rates compared to other major countries, strong capital inflows, and its status as a perceived safe haven in times of turmoil. After rising to a multi-decade high in January 2025, it declined leading up to, and then following, last year’s tariff announcements.

The dollar's real value is off its recent highs

Source: Bloomberg. U.S. Federal Reserve Trade Weighted Real Broad Dollar Index (USTRBGD Index). Monthly data as of 1/31/2026.

The U.S. Federal Reserve Trade Weighted Real Broad Dollar Index (USTRBGD Index) is a measure of the inflation-adjusted foreign exchange value of the United States dollar relative to other world currencies. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

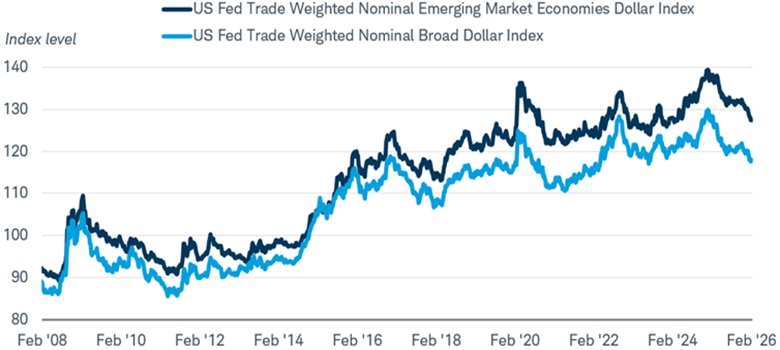

The dollar's gains—and subsequent losses—have been broad-based, with both emerging market and major developed market currencies following similar trajectories. This chart shows it in nominal terms.

Changes in the dollar have been broad-based

Source: Federal Reserve Bank of St. Louis. Weekly data from 2/20/2008 through 2/20/2026.

Nominal Broad U.S. Dollar Index, Index Jan 2006=100, Daily, Not Seasonally Adjusted and Nominal Emerging Market Economies U.S. Dollar Index, Index Jan 2006=100, Daily, Not Seasonally Adjusted. The Nominal Broad U.S. Dollar Index (Jan 2006=100, Daily, Not Seasonally Adjusted) is a measure of the nominal value of the United States dollar relative to other world currencies. The Nominal Emerging Market Economies U.S. Dollar Index (Jan 2006=100, Daily, Not Seasonally Adjusted) is a weighted average of the nominal foreign exchange value of the U.S. dollar against a subset of the broad index currencies that are emerging-market economies. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

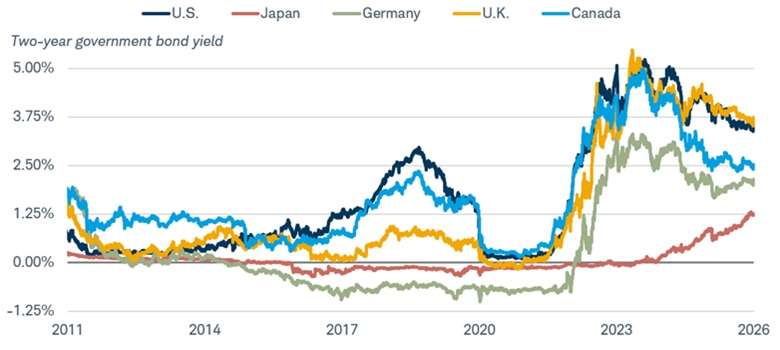

Coming out of the long stretch of lackluster growth in the aftermath of the financial crisis of 2008-2009, the dollar was largely range-bound against major currencies, but it began to move higher in 2014 as U.S. interest rates began to move up. Higher interest rates boosted returns to dollar-based investors. At that time, central banks in Europe and Japan were keeping policy rates at zero or in negative territory, while U.S. rates were positive and expected to move higher. The combination of stronger economic recovery and higher yields helped push the dollar higher.

U.S. interest rates began to move higher in 2014

Source: Bloomberg, daily data from 2/27/2011 through 2/27/2026.

U.S. (USGG2YR Index), Germany (GTDEM2Y Index), U.K. (GTGBP2Y Index), Canada (GTCAD2Y Index), Japan (GTJPY2Y Index). Past performance is no guarantee of future results. For illustrative purposes only.

Demand for the U.S. dollar is still strong

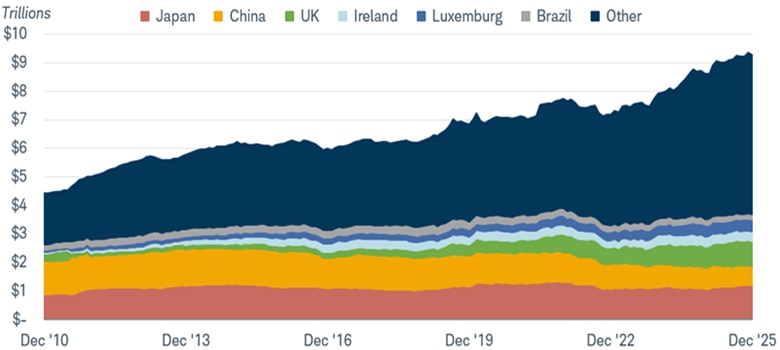

Foreign holdings of U.S. Treasury securities have been growing for years, as you can see in the chart below.

Foreign holdings of U.S. Treasuries have expanded over the past few years

Source: Bloomberg.

U.S. Treasury securities held by foreign holders for China, Japan, UK, Ireland, Luxemburg, Brazil, and Others (HOLDCH Index, HOLDJN Index, HOLDUK Index, HOLDIR Index, HOLDLU Index, HOLDBR Index). Monthly data as of 12/31/2025. This is the most recent data available for all countries.

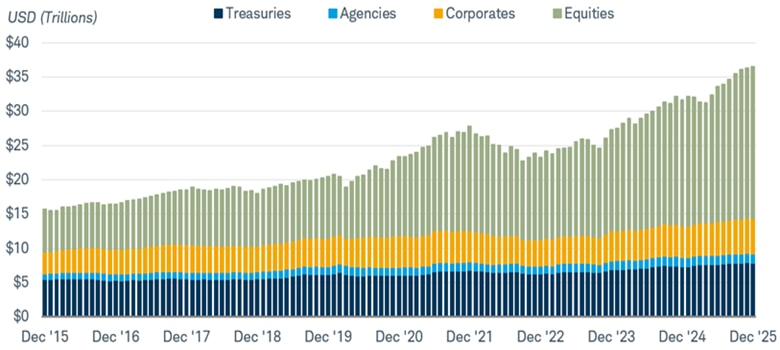

International investment flows indicate that demand for U.S. dollars extends beyond U.S. Treasury securities. With a resilient economy, the U.S. saw the largest increase in holdings—Treasuries, agencies, corporate bonds, and equities—on record in 2025. It's also worth noting that much of the rise in investment flows in the U.S. over the past few years has gone into equities.

Foreign holdings of U.S. assets

Source: Bloomberg, monthly data as of 12/31/2025.

Holdings of U.S. Long-Term Securities by Foreign Residents. U.S. Treasuries (USLTTRGR Index), U.S. Agency Bonds (USLTABGR Index), U.S. Corporate and Other Bonds (USLTCBGR Index), U.S. Corporate Stocks (USLTCSGR Index). For illustrative purposes only.

Dollar demand for transactional purposes has remained steady over the years, as well. According to the Bank of International Settlements (BIS),the dollar accounts for more than 89% of financial market transactions, as of April 2025, up from 84% in 2022. (Foreign exchange turnover adds up to 200% because there is a currency on each side of the trade.)

Dollar's reserve currency status still holding

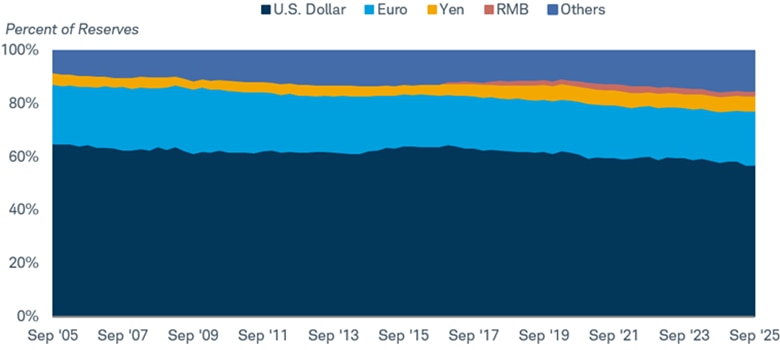

The dollar's position as the world's major reserve currency is periodically a source of concern among investors, even though its position hasn't changed much in decades. The dollar's share of global reserves has declined gradually over the past 20 years as central banks diversified their holdings, mostly into the Euro since its introduction in 1999. In September 2005, the dollar’s share of reserves was 65%, but that share dropped to 57% by September 2025. Allocations of reserves to other currencies, such as the Australian dollar and Canadian dollar, have gained modestly. Notably, the share of the Chinese renminbi was less than 2% in the third quarter of 2025.

Foreign exchange holdings by currency

Source: Bloomberg, quarterly data as of 9/30/2025.

Foreign exchange holdings as a percentage of total allocated in U.S. dollars (U.S. Dollar), the euro (Euro), the Japanese yen (Yen), the renminbi/Chinese yuan (RMB), and other reserve currencies, which are the Swiss franc, Canadian dollar, Australian dollar, British pound, and unclassified others (CCFRUSD% Index, CCFREUR% Index, CCFRJPY% Index, CCFRCNYP Index, CCFROTR% Index, CCFRCHF% Index, CCFRCADP Index, CCFRAUDP Index, CCFRGBP% Index).

There aren't currently any viable reserve-currency alternatives

A reserve currency needs to be freely convertible and have deep and liquid bond markets to be considered safe for foreign central banks to hold. Central banks need confidence that their money is easily and readily available when needed, particularly in times of stress. The U.S., with a large, open, and liquid market for Treasury securities, fits that role. That role was evident during the COVID crisis, when the U.S. Federal Reserve expanded its swap lines with foreign central banks to provide access to dollars for trade and debt payments.

While other major countries' markets have these qualities, the size and openness of the U.S. market is difficult to match. Europe's bond markets are more fragmented than the U.S. market, although a movement toward euro-denominated sovereign debt issuance would provide a stronger base for it as an attractive alternative. Japan's bond market is closely controlled by its central bank, which owns the bulk of its government debt. China has capital controls, and its currency isn't even freely convertible. Giving up capital controls would mean that the government would relinquish control over investment flows and leave the currency susceptible to decline if domestic investors moved their money elsewhere.

Some countries have begun increasing their gold reserves, but the numbers are still relatively small relative to dollar reserves. China, Russia, and India held a combined $177 billion in gold reserves through October 2025, according to the International Monetary Fund, up from $77 billion at the end of 2010. That compares to US gold reserves of just over $260 billion, which have held steady for years.

To put the numbers below into perspective, the total amount of US dollars held as foreign reserves was $7.4 trillion through the end of the third quarter of 2025.

China, Russia, and India have been increasing their gold reserves

Some of the factors supporting a strong dollar remain intact, but others may be waning. U.S. economic growth continues to outpace the rate of growth in other major developed market countries, which should be favorable for the dollar.

Interest rate differentials could mean less support for the dollar going forward, however. The yield advantage of the Bloomberg US Aggregate Index over the Bloomberg Global Aggregate ex-USD Index fell to 1.4% in late February, down from a 2.4% advantage in January 2025. The Federal Reserve is likely to cut rates further later this year, but the European Central bank is widely expected to hold rates steady this year, with rate hike expected by the Bank of Japan. Interest rate differential may continue to tighten and could put downward pressure on the dollar.

Tariffs remain a wild card. The tariff announcement in early 2025 was a key driver of the dollar's decline last year, likely given the uncertainty the tariffs introduced. With the recent Supreme Court decision ruling that the broad tariffs used under the International Emergency Economic Powers Act (IEEPA) were unconstitutional, the outlook on trade policy appears to be uncertain again.

Summing those up, we see room for the dollar to gradually decline from here, but it may be a bumpy ride. Longer-term, movement to a multi-currency global economy is possible and could have benefits, particularly for emerging-market countries where moves in the dollar can have big effects on economic growth. However, it would require some major structural changes in many regions—such as reducing barriers to trade and investment, along with strengthening protections for investors. These changes take time and political will.

Short and long-term views on the U.S. dollar

With the potential for the dollar to gradually move lower—but not lose its reserve currency status—investors Although we don't see a major bear market in the dollar developing soon, we do believe that investors may want to consider global diversification over the long run.

Investors tend to have a home bias when it comes to bond investing, but the outlook for global bond investing is more attractive than it had been for years. Average yields still appear attractive compared to the last decade and a half. The average yield of the Bloomberg Global Aggregate ex-USD Index as of 3/4/2026, is 2.75%, a level not seen at all from mid-2011 through mid-2022. With the potential for the dollar to drop a little further—potentially pulling local currencies higher—and high yields relative to the last 15 years, introducing some non-USD international bonds can make sense today.